MARKET OVERVIEW

Equities spent the second half of May caught between two powerful forces, and the bulls won. On one side stood a genuine inflation scare, rooted in a Middle East energy shock that pushed oil sharply higher, hardened the Federal Reserve’s resistance to interest rate cuts, and revived talk of potential rate hikes. On the other side, a wave of artificial intelligence enthusiasm and resilient corporate earnings carried equities to fresh record highs. Sentiment improved further late in the stretch, when reports of a preliminary ceasefire between the United States and Iran eased fears around the Strait of Hormuz and sent crude tumbling. The result was a market that repeatedly looked past hot inflation readings and hawkish central bank commentary, with technology-led optimism ultimately overpowering geopolitical risk.

Technology set the tone. Nvidia anchored the period with another blockbuster quarter, reporting record revenue driven by surging data center demand. The company paired the results with an $80 billion buyback authorization, reinforcing confidence that AI infrastructure spending remains on a steep upward path. Even though Nvidia’s own stock slipped after the report, suppliers and peers rallied, underscoring how thoroughly AI capital spending has become the market’s central engine. The momentum helped lift the S&P 500 and Nasdaq to repeated record closes, extended the S&P 500’s weekly winning streak to eight, and broadened beyond mega cap technology into health care and smaller companies.

The economic data complicated that optimism. The Personal Consumption Expenditures (PCE) price index, the Fed’s preferred inflation gauge, rose to 3.8% for the 12 months ended April, its hottest reading in nearly three years, while core PCE, which excludes food and energy, climbed to 3.3%. The oil spike tied to the Iran conflict added to the pressure, hardening the case for patience at the Fed and reviving concern that rates could move higher if inflation proved more persistent. Consumer confidence weakened as households flagged the rising cost of living, and Treasury yields touched a one-year high before easing back late in the period. Futures markets went further, pricing rising odds of a hike and erasing expectations for any near-term easing.

ADVISOR PERSPECTIVE

Heading into June, markets continue to benefit from resilient corporate earnings, improving economic activity, and ongoing investment in artificial intelligence. At the same time, the economic backdrop has become increasingly nuanced as inflation pressures show signs of persistence while labor market conditions continue to soften. The result is an environment where growth remains intact, but the path forward for monetary policy has become less certain.

Recent economic data suggests the economy may be stabilizing after several months of slowing momentum. Composite economic indicators improved from recent lows, global leading indicators remained positive, and broader measures of activity continued to support expansion. Recession concerns have moderated compared to earlier in the year, with the economy continuing to be supported by resilient consumer spending and ongoing business investment.

The labor market, however, remains an area requiring close attention. Employment-related indicators continue to lag other areas of the economy, while personal income growth remains one of the most important variables supporting future consumer spending. Although current conditions do not point toward an imminent contraction, labor market weakness remains one of the clearest risks to the expansion should it persist.

At the same time, inflation has become increasingly difficult to ignore. While headline inflation has moderated significantly from its peak, recent data suggests the final stage of returning inflation to the Federal Reserve’s 2% target may prove more challenging than many anticipated. Bloomberg economists currently project CPI to decline from 3.9% in the second quarter of 2026 to 2.2% by mid-2027, but recent inflation readings have remained firm enough to keep investors cautious.

The persistence of inflation creates a difficult balancing act for policymakers. Under normal circumstances, softer labor market conditions would support lower interest rates. However, inflation that remains above target limits the Federal Reserve’s flexibility and increases the likelihood that policy remains restrictive for longer than markets originally expected. As a result, investors have steadily moved away from forecasting multiple rate cuts and have increasingly embraced a higher-for-longer interest rate environment. Although additional rate hikes are not the base case, the market has become more sensitive to the possibility that policy could remain restrictive, or even tighten further, if inflation proves more persistent than expected.

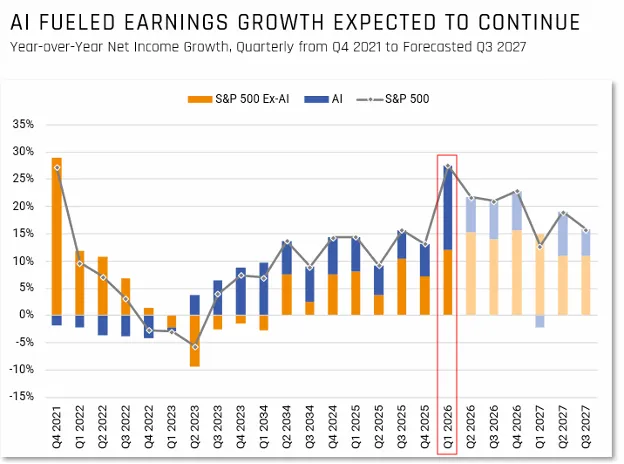

While inflation and monetary policy remain key sources of uncertainty, corporate earnings have continued to provide an important source of support for equity markets. Approximately 83% of S&P 500 companies exceeded first-quarter earnings expectations, extending a trend of stronger than anticipated profitability. Artificial intelligence remains a major driver of that strength, with just seventeen core AI-related companies generating roughly half of total S&P 500 earnings growth.

The accompanying chart highlights the growing gap between earnings growth generated by AI-related companies and the broader market. First-quarter S&P 500 earnings per share grew approximately 29%, more than double consensus expectations, with a relatively small group of AI beneficiaries contributing a disproportionate share of total profit growth. In fact, the contribution from AI-related companies represents the widest earnings growth gap in the dataset dating back to 2021.

Importantly, the strength is not solely the result of revenue growth. Record operating margins suggest that artificial intelligence is increasingly creating productivity gains and operating leverage across many of the companies leading the investment cycle. Meanwhile, earnings growth outside of the AI cohort has remained positive but considerably more moderate, highlighting the degree of concentration currently embedded within headline market results.

While concentrated leadership can raise concerns about market breadth, the earnings results themselves continue to demonstrate the powerful impact technology and innovation are having across the economy. As long as earnings expectations continue to be met or exceeded, AI-related companies are likely to remain an important source of support for broader equity markets. At the same time, investors should recognize that markets may become increasingly sensitive to any slowdown in earnings growth from this relatively small group of leaders.

Another notable development during the month was the behavior of traditional defensive assets. Gold declined approximately 12% despite ongoing geopolitical tensions and elevated energy prices. Rising Treasury yields, which increased roughly 35 basis points during the period, a stronger U.S. dollar and changing patterns of sovereign demand all contributed to the move. The episode served as a reminder that market relationships can evolve as economic conditions change and that historical patterns do not always repeat themselves.

Taken together, the current environment points to a market supported by earnings growth, economic resilience, and continued innovation, but one that may become increasingly sensitive to inflation data and Federal Reserve communications. While volatility may emerge as investors reassess interest rate expectations, the fundamental backdrop remains constructive.

In that context, maintaining diversification, emphasizing quality investments, and remaining disciplined through periods of uncertainty remain as important as ever. Inflation, employment, and monetary policy will likely continue to dominate headlines throughout the second half of the year, but successful investing remains rooted in balancing opportunity with risk management and maintaining a long-term perspective through changing market environments.

DISCLOSURE

This update is not intended to be relied upon as forecast, research, or investment advice, and is not a recommendation, offer, or solicitation to buy or sell any securities or to adopt any investment opinions expressed are as of the date noted and may change as subsequent conditions vary. The information and opinions contained in this letter are derived from proprietary and nonproprietary sources deemed by Hilltop Wealth & Tax Solutions to be reliable. The letter may contain “forward-looking” information that is not purely historical in nature. Such information may include, among other things, projections, and forecasts. There is no guarantee that any forecast made will materialize. Additional information about Hilltop Wealth & Tax Solutions is available in its current disclosure documents, Form ADV, Form ADV Part 2A Brochure, and Client Relationship Summary Report which are accessible online via the SEC’s Investment Adviser Public Disclosure (IAPD) database at www.adviserinfo.sec.gov, using SEC # 801-115255. Hilltop Wealth & Tax Solutions is neither an attorney nor an accountant, and no portion of this content should be interpreted as legal, accounting, or tax advice.