MARKET OVERVIEW

Equity markets were pulled in opposite directions as the second quarter drew to a close. On one side, a newly hawkish Federal Reserve and the firmest inflation readings in three years argued for caution. On the other, a tentative easing of the conflict between the U.S. and Iran pulled oil prices sharply lower and revived appetite for risk. Technology shares, buoyed by the relentless buildout of artificial intelligence infrastructure, did much of the heavy lifting, helping equities recover from a mid-month slide and close out one of their strongest quarters in years. The result was a choppy stretch that nonetheless ended on firmer footing.

The energy picture shifted quickly as a preliminary deal opened a 60-day negotiating window and raised hopes that the Strait of Hormuz would reopen. Brent crude oil slid to roughly $73.50 a barrel, and West Texas Intermediate dipped just below $70, both their lowest levels since the war began. Cheaper oil eased a key inflation worry and lifted sentiment into quarter-end. Technology led the rebound, and the Dow Jones Industrial Average notched its first close above 52,000 on June 29. The milestone coincided with Alphabet’s debut in the index, replacing Verizon after 22 years and deepening the Dow’s tilt toward Big Tech. The S&P 500 and Nasdaq, while below their early-June peaks, still secured their best quarter since 2020.

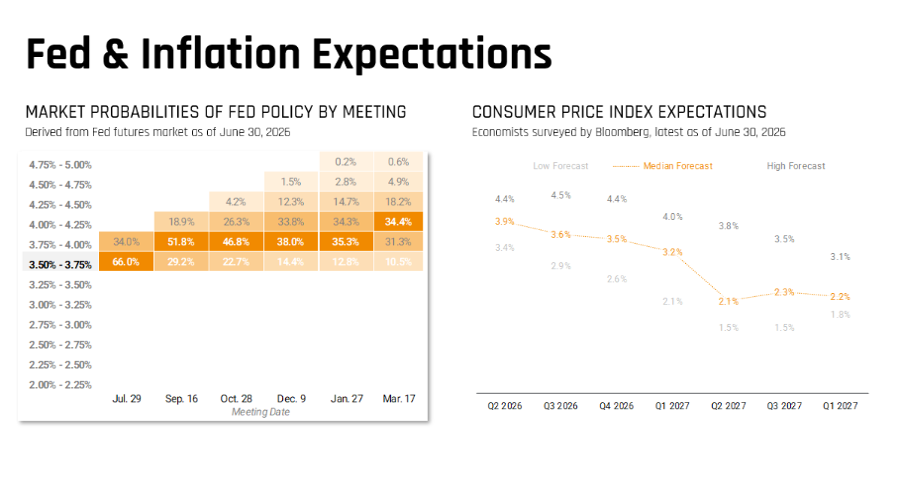

Policy and prices took center stage at midmonth. At Kevin Warsh’s first meeting as chair, the Fed held its benchmark rate at 3.50% to 3.75% on June 17 but delivered a hawkish surprise, lifting its median year-end projection to 3.8% and signaling that at least one rate hike this year is now on the table. The data reinforced that stance. The Personal Consumption Expenditures (PCE) price index, the Fed’s preferred gauge, rose 4.1% in the 12 months through May, its highest in three years, while core PCE, which excludes food and energy, climbed 3.4%. Resilient growth gave officials room to wait: the third estimate of first-quarter gross domestic product was revised up to 2.1%, and jobless claims eased to around 215,000. With a packed July ahead, including the July 24 expiration of the 10% global tariff, a Federal Reserve meeting, and the start of second-quarter earnings, investors will be watching whether firm inflation or the recent relief in oil and geopolitics sets the tone for the second half.

Advisor Perspective

As the second half of 2026 begins, the investment landscape remains defined by a balance between improving fundamentals and ongoing policy uncertainty. Markets have continued to demonstrate remarkable resilience despite geopolitical unrest, shifting interest rate expectations, and periodic bouts of volatility. Rather than signaling a deterioration in the broader outlook, recent market behavior reflects an environment in which investors are increasingly distinguishing between short-term headlines and longer-term economic trends.

Recent economic data has provided further evidence that conditions continue to stabilize. Consumer activity strengthened during June, while global output and other forward-looking indicators improved, reinforcing the view that underlying economic momentum continues to build. Employment remains one of the weaker areas of the economy, but broader measures of business activity and demand have remained resilient, supporting the view that the economy continues to stabilize despite ongoing policy uncertainty. Although inflation has yet to fully return to the Federal Reserve’s target, median economist forecasts continue to suggest gradual progress over the coming year. At the same time, markets have largely accepted that policymakers may not be finished tightening monetary policy, with an additional rate increase remaining a realistic possibility later this year.

Even as broader economic conditions continue to improve, inflation remains one of the most important variables shaping the investment outlook. While price pressures have moderated significantly from their 2022 peak, recent data suggests the final stage of returning inflation to the Federal Reserve’s 2% target may prove more gradual than many investors expected. Economist forecasts continue to project inflation steadily declining toward target over the next year, but recent readings have remained firm enough for policymakers to maintain a cautious stance. As a result, markets have increasingly embraced a higher-for-longer interest rate environment, recognizing that the Federal Reserve is likely to prioritize sustained progress on inflation before considering any meaningful shift in monetary policy.

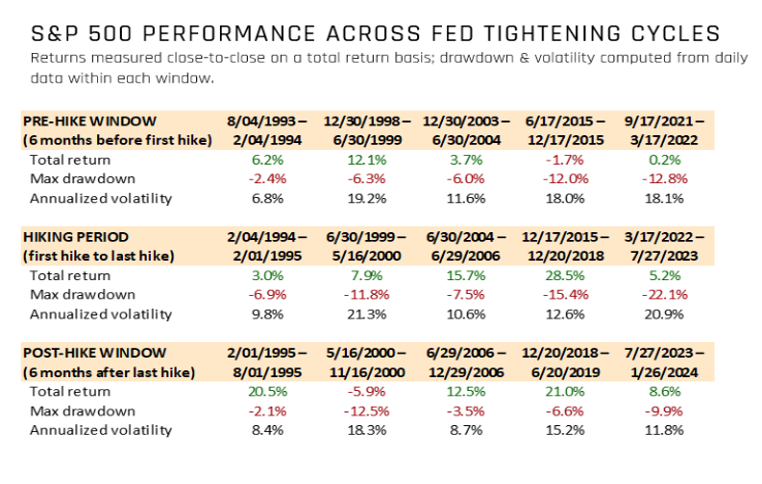

With markets increasingly pricing in the possibility of additional policy tightening, it is helpful to view the current environment through a historical lens. The prospect of higher interest rates often raises concern among investors, but history suggests the relationship between monetary tightening and equity performance is more nuanced than many assume.

The accompanying chart highlights S&P 500 performance across the five Federal Reserve tightening cycles since 1994. While each period experienced varying levels of volatility and temporary drawdowns, equities generated positive returns during every hiking cycle, averaging approximately 12.1%. The data reinforces an important principle for long-term investors: higher interest rates may create periods of uncertainty, but they have not historically prevented fundamentally healthy markets from advancing over time. Although the current cycle could include one or two additional rate increases, history suggests that disciplined portfolio management has generally proven more effective than reacting to short-term policy changes.

Beyond the macroeconomic backdrop, corporate fundamentals continue to provide meaningful support for markets. Artificial intelligence remains an important long-term investment theme, but the conversation is gradually evolving. Earlier this year, a relatively small group of AI-driven companies accounted for an outsized share of market gains. More recently, improving earnings across a broader range of industries and expanding market participation have begun to complement that leadership. This broadening of returns is generally considered a healthy development, reducing reliance on any single sector while creating additional opportunities across diversified portfolios.

While uncertainty surrounding inflation, monetary policy, and global events is likely to persist, the broader backdrop continues to support a disciplined, long-term investment approach. Economic fundamentals have shown steady improvement, market participation has broadened, and corporate earnings remain resilient despite periodic volatility. Although short-term headlines will continue to influence day-to-day market movements, history consistently demonstrates that maintaining a diversified portfolio and focusing on long-term objectives has been a more reliable strategy than attempting to anticipate each policy decision or market swing. As the second half of the year unfolds, investors should remain prepared for continued volatility while recognizing that periods of uncertainty have often created opportunities for patient, disciplined investors.

DISCLOSURE

This update is not intended to be relied upon as forecast, research, or investment advice, and is not a recommendation, offer, or solicitation to buy or sell any securities or to adopt any investment opinions expressed are as of the date noted and may change as subsequent conditions vary. The information and opinions contained in this letter are derived from proprietary and nonproprietary sources deemed by Hilltop Wealth & Tax Solutions to be reliable. The letter may contain “forward-looking” information that is not purely historical in nature. Such information may include, among other things, projections, and forecasts. There is no guarantee that any forecast made will materialize. Additional information about Hilltop Wealth & Tax Solutions is available in its current disclosure documents, Form ADV, Form ADV Part 2A Brochure, and Client Relationship Summary Report which are accessible online via the SEC’s Investment Adviser Public Disclosure (IAPD) database at www.adviserinfo.sec.gov, using SEC # 801-115255. Hilltop Wealth & Tax Solutions is neither an attorney nor an accountant, and no portion of this content should be interpreted as legal, accounting, or tax advice.