MARKET OVERVIEW

U.S. equities spent much of the past two weeks caught between competing forces before a dramatic escalation in the Middle East reshaped the landscape entirely. The S&P 500 traded in a narrow range around the 6,900 level for most of the period, weighed down by sticky inflation data and lingering concerns about AI-driven disruption in the software sector. That uneasy calm shattered on February 28, when coordinated U.S. and Israeli strikes on Iran killed Supreme Leader Ali Khamenei and sent shockwaves through global markets. Brent crude oil prices spiked, and gold jumped to near $5,400 per ounce as markets began pricing in the geopolitical risk.

The geopolitical shock compounded what had already been a turbulent stretch. Software stocks continued their steep repricing as fears grew that agentic AI tools could structurally erode traditional SaaS business models, a selloff Wall Street has dubbed the “SaaSpocalypse.” Nvidia’s fiscal fourth-quarter earnings offered a counterpoint, with revenue of $68.1 billion topping expectations. But even that beat failed to lift broader sentiment, as investors weighed the widening divide between AI infrastructure winners and sectors facing disruption. Brent crude closed around $72/barrel on Friday before the strikes, already up roughly 19% year to date. Analysts project prices could spike by $10 to $20, particularly if Iran follows through on threats to close the Strait of Hormuz, a chokepoint for roughly 20% of global oil supply.

On the economic front, the January Producer Price Index (PPI) surprised to the upside, rising 0.5% versus the 0.3% forecast. Core PPI, which excludes food and energy, jumped 0.8%, well above consensus. The data raised concerns ahead of the January Personal Consumption Expenditures (PCE) report, due March 13, as several PPI components feed directly into the Fed’s preferred inflation gauge. Those inflation worries now take on added urgency given the potential for an oil-driven price shock. The Supreme Court on February 20 struck down tariffs imposed under IEEPA by a 6-3 vote, though the administration pivoted to alternative legal authorities, leaving trade policy uncertain.

ADVISOR PERSPECTIVE

Entering March 2026, investors are navigating a market shaped by geopolitical uncertainty, evolving monetary policy expectations, and a recalibration within parts of the technology sector tied to artificial intelligence. While global tensions and shifting interest rate outlooks have contributed to periods of volatility, the broader market backdrop remains relatively stable. Economic growth in the United States continues at a moderate pace, and inflation has continued to ease, but policymakers remain cautious about declaring victory. Markets entered the year expecting the Federal Reserve to delay rate cuts until later in 2026, and recent developments—including renewed energy price pressures—have reinforced the likelihood that any easing cycle will be gradual and data dependent rather than immediate.

Recent geopolitical developments have once again pushed energy markets into focus. Rising tensions between the United States and Iran have lifted oil prices, with Brent crude approaching the high-$70s per barrel. Analysts estimate that current tensions have added a meaningful geopolitical risk premium to oil prices as markets factor in potential supply disruptions in the Middle East. Shipping routes through key waterways and broader regional instability continue to introduce uncertainty into energy markets, though global supply buffers remain intact due to OPEC spare capacity and alternative export channels.

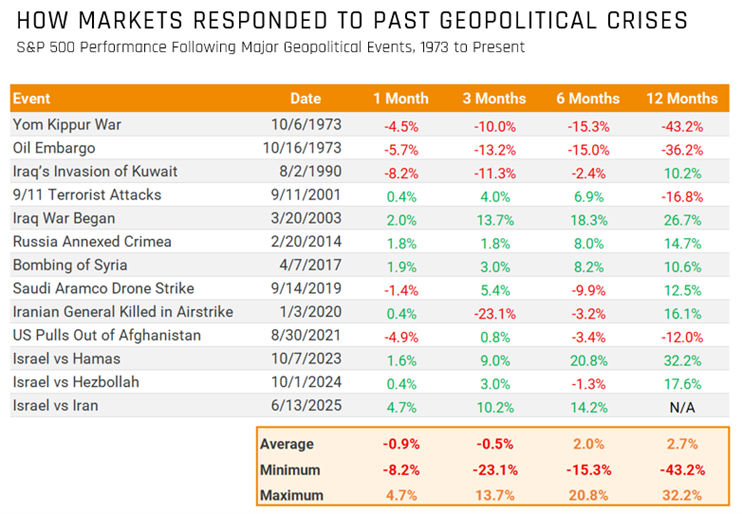

Historically, markets have shown an ability to absorb geopolitical shocks over time. Initial reactions often include heightened volatility and short-term declines as investors digest uncertainty. However, looking across major geopolitical events over the past several decades, equity markets have typically recovered in the months following these events. Average returns following geopolitical crises have been slightly negative in the immediate aftermath but have generally turned positive over six- and twelve-month horizons. This pattern reinforces the idea that geopolitical events tend to influence short-term sentiment more than long-term economic trajectories.

Inflation risk from higher oil prices also appears smaller than headlines suggest. Research from the Federal Reserve finds that even a severe oil shock would add just 1.3 percentage points to headline inflation, with effects fading within a year. While spikes in energy prices can temporarily slow the pace of disinflation, the broader trend in price pressures remains relatively stable. For policymakers, the key challenge is balancing continued progress on inflation with signs that economic growth may gradually moderate as restrictive monetary policy continues to work through the economy.

The outlook for monetary policy remains one of the most closely watched themes in markets. After a period of restrictive interest rates, investors are increasingly focused on the potential for rate cuts later in 2026. While inflation has gradually moved closer to the Federal Reserve’s target, policymakers remain cautious as energy prices and other factors could slow the pace of disinflation. As a result, central banks may begin shifting toward a more neutral policy stance in the second half of the year, though markets are currently pricing in a gradual easing cycle rather than an aggressive series of cuts.

Lower interest rates, if realized, could provide support for both equity markets and interest-sensitive sectors such as housing and capital investment. However, the path toward rate cuts will likely remain data-dependent. Renewed inflation pressures from energy prices, supply disruptions, or stronger-than-expected wage growth could delay the start of monetary easing. As a result, markets are likely to remain highly sensitive to incoming economic data, particularly labor market conditions and inflation trends.

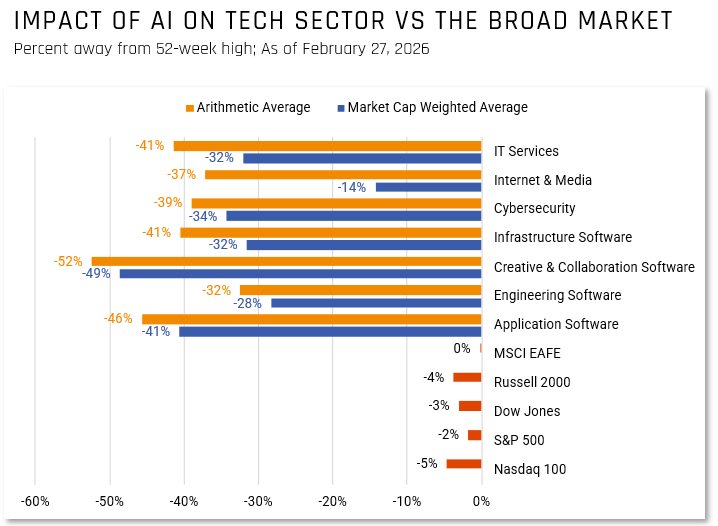

Within equity markets, AI-focused technology segments have seen some of the sharpest pullbacks from their 52-week highs. Areas such as creative and collaboration software and application software have declined more than 40%, while cybersecurity, infrastructure software, and IT services have also experienced meaningful corrections. These declines reflect a shift in investor expectations following a period in which AI-related companies saw rapid valuation expansion as markets priced in transformative productivity gains and long-term revenue growth.

Importantly, this volatility has remained concentrated in specific technology subsectors rather than spreading across the broader market. Major benchmarks such as the S&P 500 and Dow Jones remain much closer to their highs compared with the steep drawdowns seen in AI-exposed industries. This divergence suggests the current selloff is better characterized as a repricing of AI expectations rather than a sign of systemic weakness in the overall economy.

Diversified portfolios have therefore been largely insulated from the sharp volatility within individual technology segments. Investors with exposure across sectors, including healthcare, industrials, financials, and energy, have experienced more stable performance than those concentrated heavily in software and internet companies tied to AI development.

Stepping back, the current market environment reflects a complex but manageable mix of factors. Geopolitical tensions have introduced uncertainty in energy markets, but historical precedents suggest that markets typically recover from these events over time. Meanwhile, the AI sector is undergoing a recalibration after a period of extraordinary enthusiasm, leading to greater dispersion in returns across technology subsectors.

For long-term investors, the broader lesson is that market narratives often shift more quickly than underlying economic fundamentals. While volatility tied to geopolitics, interest rates, or technological disruption may continue in the near term, diversified portfolios and disciplined investment strategies remain well-positioned to navigate the evolving market landscape.

This update is not intended to be relied upon as forecast, research, or investment advice, and is not a recommendation, offer, or solicitation to buy or sell any securities or to adopt any investment opinions expressed are as of the date noted and may change as subsequent conditions vary. The information and opinions contained in this letter are derived from proprietary and nonproprietary sources deemed by Hilltop Wealth & Tax Solutions to be reliable. The letter may contain “forward-looking” information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecast made will materialize. Additional information about Hilltop Wealth Solutions is available in its current disclosure documents, Form ADV, Form ADV Part 2A Brochure, and Client Relationship Summary Report, which are accessible online via the SEC’s Investment Adviser Public Disclosure (IAPD) database at www.adviserinfo.sec.gov, using SEC # 801-115255. Hilltop Wealth Solutions is neither an attorney nor an accountant, and no portion of this content should be interpreted as legal, accounting, or tax advice.