MARKET UPDATE

Markets finished the year with a familiar mix of resilience and late-December caution. U.S. stocks hovered near record levels even as the final sessions turned choppy, reflecting profit-taking and thinner holiday liquidity more than any single shock. Globally, equities capped another strong year, supported by rate-cut expectations, solid earnings momentum, and continued investment tied to AI-related spending—while concentration in a handful of mega-cap leaders remained a defining feature of index performance.

Borrowing costs eased as cooler inflation met a more cautious Federal Reserve. A downside surprise in inflation, with CPI at 2.7% year-over-year and core CPI at 2.6%, helped push Treasury yields lower and reinforced expectations for a slower pace of rate cuts in 2026. At the same time, minutes from the Fed’s December meeting revealed meaningful disagreement around the recent quarter-point cut and stressed that any further easing will be data-dependent rather than pre-set. Those moves flowed into housing: as longer-term yields drifted down, the average 30-year fixed mortgage rate fell to roughly 6.15%, providing a modest tailwind for rate-sensitive sectors.

Overall, the latest U.S. data reinforced the idea that growth is moderating, but the expansion remains intact. The delayed third-quarter GDP report showed the economy growing at a 4.3% annualized pace, supported by consumer spending, though activity appeared to cool into year-end. At the same time, the labor market continued to lose some steam without showing signs of broad stress: weekly jobless claims slipped to 199,000, layoffs remained historically low, and the unemployment rate ticked up to 4.6% in November amid slower hiring. Taken together, the picture points to a late-cycle slowdown rather than an abrupt break, raising the new year’s key question: how smoothly inflation can keep easing as growth and jobs gradually cool.

The bottom line: The market closed the year pricing a “cooling-but-still-growing” baseline: inflation appears to be easing, the labor market is loosening gradually, and policy is shifting from restrictive toward more neutral, though not without debate. The key swing factors heading into the new year are whether disinflation continues without a sharper slowdown in jobs, and whether the rally broadens beyond the crowded themes that drove 2025’s gains.

ADVISORS PERSPECTIVE

As 2025 drew to a close, the broader economic and market environment carried a tone that was more resilient and fundamentally supported than many expected earlier in the year, even as investors continued to navigate a slowing economic backdrop and late-cycle pressures. While concerns around inflation, policy direction, and global growth persisted at various points throughout the year, markets demonstrated a notable ability to absorb uncertainty and re-establish momentum. U.S. equities capped the year with 39 new all-time highs in the S&P 500, the sixth most this century. The dispersion of all-time highs throughout the year was not symmetrical, with the majority occurring in the second half of the year, following the recovery from the tariff implementation.

Looking ahead, we remain cautious as 2026 is forecasted to be a year of moderation, not recession. Consensus projections cluster around modest growth in the U.S. and worldwide, with unemployment inching up but not surging, inflation continuing its gradual descent, and central banks moving cautiously on further cuts until incoming data justify action. The story for markets in 2026 is likely to be one of continued resilience supported by strong corporate earnings, technological investment, and fiscal and monetary policy that balances growth with price stability — but with the important caveat that risks are abundant.

At the corporate level, earnings strength remained one of the most important anchors for market performance in 2025. Profitability consistently exceeded expectations across a broad range of sectors, reinforcing a key theme of this cycle: companies have become structurally more efficient. Long-term shifts toward automation, AI-enabled productivity, and scalable business models have allowed firms to defend margins even as growth moderated. These dynamics have supported elevated valuations and helped markets remain grounded in fundamentals despite ongoing macro uncertainty.

Recession monitoring indicators remain constructive and point more toward deceleration than contraction as the calendar turns. Measures such as real personal income, real personal consumption, retail sales, non-farm payrolls, and industrial production have shown volatility throughout the year, but the aggregate trend remains expansionary. While growth has slowed meaningfully from prior peaks, the absence of broad, sustained deterioration suggests the economy is transitioning into a late-cycle phase rather than entering a recession. This distinction remains central to the outlook for 2026.

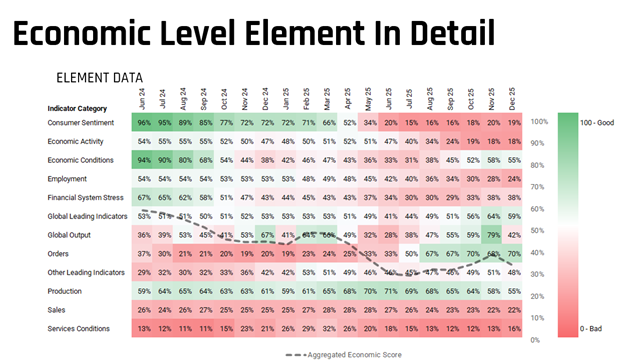

The economic element data highlights a clear divergence between market resilience and underlying confidence and labor trends. Consumer sentiment has deteriorated sharply over the past year, falling from elevated levels in mid-2024 to deeply depressed readings by the end of 2025, underscoring ongoing affordability pressures and fragile household confidence. Employment indicators have also weakened steadily, reflecting slower hiring and a cooling labor market, though not yet signaling broad-based stress. Global output has been notably volatile, improving later in the year before dropping meaningfully in December, reinforcing concerns about uneven international growth.

These dynamics have contributed to a growing concern that markets may be ahead of the economy. Equity prices appear to be discounting a relatively smooth path forward with continued disinflation, steady earnings growth, and a policy environment that becomes incrementally less restrictive. The economy, by contrast, is navigating slower growth, weaker confidence, and late-cycle pressures. This disconnect does not suggest markets are fundamentally misaligned, but it does imply that expectations are elevated and that sensitivity to economic data may increase as markets work to reconcile price with fundamentals.

Monetary policy remains an important, but not dominant, factor in shaping the path ahead. Inflation progress allowed the Federal Reserve to begin cutting rates late in 2025, signaling a move away from peak restrictiveness. Looking into 2026, expectations for additional cuts have become more measured. Rather than anticipating an aggressive easing cycle, markets are pricing a gradual adjustment, with longer-term rates settling above pre-pandemic norms. Mortgage rates in the mid-single digits and policy rates in a higher neutral range are increasingly viewed as realistic, reinforcing the idea that future returns will be driven more by earnings and economic activity than by policy tailwinds.

In summary, the market enters 2026 following a year defined by resilience amid economic moderation. The achievement of 39 all-time highs underscores the durability of corporate earnings and improving financial conditions, while recession indicators continue to point toward slowing, but ongoing growth. At the same time, softer employment trends, fragile consumer sentiment, and uneven global output argue for a measured and cautious approach. As the cycle matures, the market environment increasingly favors patience, selectivity, and a focus on fundamentals as growth and valuations work toward better alignment.

This update is not intended to be relied upon as forecast, research, or investment advice, and is not a recommendation, offer, or solicitation to buy or sell any securities or to adopt any investment opinions expressed are as of the date noted and may change as subsequent conditions vary. The information and opinions contained in this letter are derived from proprietary and nonproprietary sources deemed by Hilltop Wealth & Tax Solutions to be reliable. The letter may contain “forward-looking” information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecast made will materialize. Additional information about Hilltop Wealth Solutions is available in its current disclosure documents, Form ADV, Form ADV Part 2A Brochure, and Client Relationship Summary Report, which are accessible online via the SEC’s Investment Adviser Public Disclosure (IAPD) database at www.adviserinfo.sec.gov, using SEC # 801-115255. Hilltop Wealth Solutions is neither an attorney nor an accountant, and no portion of this content should be interpreted as legal, accounting, or tax advice.