MARKET OVERVIEW

March has been one of the most turbulent months for financial markets in recent memory. A confluence of geopolitical disruption, shifting monetary policy expectations, and unusual cross-asset behavior has left investors navigating unfamiliar terrain. The S&P 500 finished March down 5%, its worst month since 2022, capping a quarter in which all three major indexes posted meaningful losses. At its lowest point, the index sat roughly 9% below its late-January all-time high after five consecutive weekly declines. A sharp rally on the final trading day, sparked by reports that the Iranian President was open to ending the conflict, lifted the broad market nearly 3% and provided a jolt of relief, though it barely dented the monthly damage.

The war in Iran, now in its second month, continued to overshadow everything else. The effective closure of the Strait of Hormuz, through which roughly 20% of global oil supply normally flows, kept oil prices elevated and volatile. A coordinated release of 400 million barrels from global strategic reserves helped contain a further spike but could not resolve the underlying disruption. As a result, U.S. gas prices crossed $4 per gallon for the first time since 2022. Energy was the lone bright spot in an otherwise dismal market, with the S&P 500 Energy Index surging 39% for the quarter and outpacing every other sector by a historic margin.

The Federal Reserve held its benchmark rate steady at 3.5% to 3.75%, citing elevated uncertainty from the conflict. Updated projections raised the 2026 inflation outlook to 2.7% and still penciled in one rate cut this year, but a growing number of officials now expect no reductions at all. Chair Powell acknowledged that surging oil could weigh on growth but said it was too early to gauge the war’s full economic impact. The January Personal Consumption Expenditures (PCE) report reinforced that caution, with core PCE, which excludes food and energy, running at 3.1% year over year, well above the Fed’s 2% target. The path forward hinges on the conflict’s resolution. Until energy markets stabilize, geopolitical risk and rate-cut expectations will continue to drive sentiment.

ADVISOR PERSPECTIVE

Global financial markets closed the first quarter of 2026 under a noticeably heavier tone, with geopolitical risk rapidly overtaking previously stabilizing macro trends. The war involving Iran has quickly become the dominant force shaping market sentiment, shifting investor focus away from a previously improving inflation backdrop toward a more complex and concerning mix of risks. What initially appeared to be a contained regional conflict now carries broader implications, particularly through its influence on global energy markets and trade stability. The possibility of prolonged disruption, especially around key transit points like the Strait of Hormuz, has introduced a layer of uncertainty that markets are still struggling to fully price.

The market response to the Iran conflict has evolved from an initial risk-off reaction into a more persistent repricing of geopolitical uncertainty. Energy markets, in particular, are now embedding a sustained risk premium, as investors weigh not just current supply disruptions but the potential for intermittent outages, escalation, or broader regional involvement. This has translated into heightened volatility across asset classes, with equities struggling to maintain direction and bond markets oscillating between inflation concerns and slowing growth expectations. Importantly, the uncertainty is not tied to a single outcome, but to a wide range of plausible scenarios, from partial de-escalation to prolonged disruption of critical shipping lanes. That range itself is what markets are finding difficult to absorb. As a result, pricing has become more reactive and less anchored, with sentiment shifting quickly alongside headlines. Until there is greater clarity on the duration and scope of the conflict, this elevated level of uncertainty is likely to remain a defining feature of the market environment, continuing to cloud the outlook for both inflation and growth.

At the same time, history suggests markets tend to adjust to oil shocks over time, though not without meaningful near-term volatility. In 4 of the last 5 major Middle East disruptions, the S&P 500 was higher one year later, and supply shocks have typically resolved within months as higher prices incentivize increased production and alternative transport routes. Early signs of that adjustment are already emerging, with partial supply rerouting helping offset losses, though not fully closing the gap. The challenge for markets is reconciling this pattern of eventual stabilization with a current shock that remains unresolved, leaving investors caught between expectations of normalization and the risk of a more prolonged disruption.

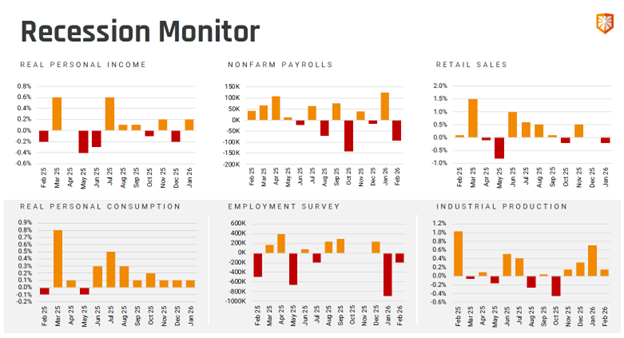

Beneath the surface, economic conditions are showing clearer signs of strain, particularly on the consumer side. March data pointed to a noticeable deterioration in employment trends, alongside a decline in broader measures of economic activity and production. Household sentiment, while ticking slightly higher, remains deeply subdued by historical standards, underscoring a lack of confidence in the near-term outlook. Spending activity has also failed to provide a meaningful offset, with demand largely stagnant rather than expanding.

At the same time, the picture is not uniformly negative. Forward-looking indicators continue to offer a degree of support that complicates the narrative of outright deterioration. Measures tied to future global activity remain relatively steady, with improvements in order flow and strength in service-sector conditions pointing to underlying demand that has not fully broken down. Even global output, while easing modestly from prior levels, continues to hold at a comparatively firm level. This divergence suggests an economy that is under pressure but not yet contracting in a broad or synchronized way. Instead, it reflects a period of tension where fragility is building, but a full downturn has not yet taken hold.

The recession monitor presents a notably uneven picture of the economy, with key indicators sending conflicting signals rather than pointing to a clear trend. Measures tied to income and consumption remain relatively stable to modestly positive in recent months, suggesting that household fundamentals have not fully broken down. At the same time, labor market data appears far more volatile, with sharp swings in both nonfarm payrolls and employment survey figures, including several deeply negative readings that raise concern about underlying softness. Taken together, the data does not point to a synchronized downturn, but rather an economy lacking cohesion, making the overall trajectory increasingly uncertain.

One potential area of support for markets in the near term, however, is the upcoming earnings season, which could provide a more constructive counterbalance to the broader macro uncertainty. Despite rising input costs and geopolitical pressures, many companies have entered this period with relatively strong balance sheets and stable demand in key segments, particularly within services and higher-margin industries. There is also the possibility that expectations have been reset lower in recent weeks, creating room for positive surprises if results come in even modestly ahead of forecasts. Forward guidance will be especially important, as it may offer clearer insight into how businesses are navigating cost pressures and demand trends. While risks remain, a better-than-expected earnings season could help stabilize sentiment and provide a temporary anchor for markets that have otherwise been driven by external uncertainties.

Against this backdrop, the outlook has become increasingly concerning, with markets lacking a clear anchor as geopolitical risk, mixed weakening economic signals, and policy ambiguity converge. While areas of resilience remain, they are being offset by signs of emerging weakness, leaving the overall trajectory difficult to define. The path forward will depend heavily on how these forces evolve, whether geopolitical tensions ease and data stabilizes, or whether current pressures begin to compound. Until then, markets are likely to remain unsettled, with sentiment shifting quickly and conviction remaining limited.

This update is not intended to be relied upon as forecast, research, or investment advice, and is not a recommendation, offer, or solicitation to buy or sell any securities or to adopt any investment opinions expressed are as of the date noted and may change as subsequent conditions vary. The information and opinions contained in this letter are derived from proprietary and nonproprietary sources deemed by Hilltop Wealth & Tax Solutions to be reliable. The letter may contain “forward-looking” information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecast made will materialize. Additional information about Hilltop Wealth Solutions is available in its current disclosure documents, Form ADV, Form ADV Part 2A Brochure, and Client Relationship Summary Report, which are accessible online via the SEC’s Investment Adviser Public Disclosure (IAPD) database at www.adviserinfo.sec.gov, using SEC # 801-115255. Hilltop Wealth Solutions is neither an attorney nor an accountant, and no portion of this content should be interpreted as legal, accounting, or tax advice.